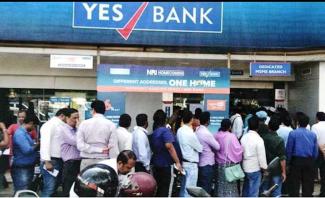

WITHIN a few months of the PMC bank collapse, another bank- Yes Bank which is now being jokingly called ‘No Bank’ crumbled. But the fear in banking sector in general doesn’t subside here, as most Public Sector Banks (PSBs) have posted in red in last two financial years. The total loans written off in last financial year by banks stood at Rs 2.54 lakh Crore, 20% of all their NPAs. (Economic Times) As per earlier report combined bank write off between 2014 and 2018 stood at Rs 5.7 lakh crore worth of bad loans. Thus total bank write offs from 2014 when Modi Govt assumed power to last financial year for which data is available stands at staggering Rs 8.24 Lakh Crore, mega loot which should draw people’s attention. For PSBs loans written of is four times of their own write-offs in 2014-15. (Business Standard).

Total Write offs under Modi dispensation stands at staggering Rs 8.24 lakh Crore

Write offs jumped four times for PSBs under Modi regime

The further dipping of economic growth to 4.7% in third quarter of current financial year would certainly stress the pains of banking and financial sector as many otherwise genuinely good assets would become NPA’s especially in small and medium segments due to economic downturn. Tanking of stock market at record historic speed now would only make situation worse as investors flee for safety of capital. Corona pandemic would also certainly affect the economy now amidst news of complete shutdown doing the rounds and it is in this overall backdrop that what happened at Yes Bank should be analyzed and not as one-off incident. The news certainly is not isolated in banking and non-banking financial sector as we have seen crisis of IL & FS, Diwan housing, IDBI, Laxmi Vilas Bank besides PMC hitting the headlines only in span of last one year. Yes Bank fiasco is both fraud in lending’s at end of management of the bank headed by Rana kapoor, who is now under arrest and face criminal charges for financial irregularities, cheating etc., but more importantly structural and regulatory failure at end of RBI, Govt, auditors etc, who are supposed to push red danger button before things go out of hand.

Yes Bank third quarter numbers: Worse than what was imagined

As expected the third quarter results of Yes Bank which came out after govt declared restructuring plan, underlines the severity of crisis in the bank. For the quarter ended December 2019, Yes Bank reported a loss of Rs 18,564 Crore compared to a profit of Rs 1001 Crore in the same quarter last year. The bank’s net loss would have been wider at Rs 24,778 Crore in the third quarter, if it weren’t for a tax write back of Rs 6,214 crore. The bank reported a surge in bad loan which led to a jump in provisions that needs to be set aside against the soured debt. Gross NPA’s rose to Rs 40,709.20 Crore, or 18.87 percent of the bank’s total loan book in December quarter. (Bloomberg quint)

Union Cabinet has approved a restructuring plan for Yes Bank but success of any restructuring plan would essentially depend on success in recovery of doubtful loans and winning back confidence of depositors. It is here that we need to understand the reasons of failure in repayments on part of borrowers, recovery process, substantial increase in write-offs and bank frauds which has been taking place under Modi dispensation for banking sector in general and Yes Bank in particular. It is also essential that we analyze the restructuring plan from point of view of innocent defaulters as they are the worst hit without any fault of theirs in any of such banking fiasco.

YES BANK:

Loss of whopping Rs 18,564 Crore in December quarter

Gross NPA’s stand at Rs 40,709 Crore, around 19% of total loan book

Loan Book of Yes Bank jumped from Rs 55,000 Crore in 2014 to whopping Rs 2,41,000 Crore in 2019

Just Anil Ambani and Subhash Chandra in total defaulted to the tune of around Rs 21,000 Crore

Compromised Credit Culture in form of political impunity, reason for record increase in NPA’s

The protagonist of Modi Govt has been arguing that the NPA’s are legacy issues bestowed upon them due unhindered lending during UPA era. While this is purely an attempt to avoid political responsibility, it also fails to take into account the fact that NPA by definition arises in first place when any installments for loan repayment remains unpaid for more than ninety days. One need to raise the pertinent question that why the same financial assets which was being repaid earlier as per the agreed terms started remaining unpaid when Modi government resumed power to fix accountability? It can be for two reasons- First the genuine one where the assets which were otherwise good assets became bad due to economic downturn attributed to disastrous economic policies like demonetization and GST of Modi Govt. Whose political responsibility is this if good assets became bad because of this reason? Second is case of willful big defaulters who sees that the new Modi government will give them political cover even if they willfully default on repayments of loan. They are the once for whom Ex-Governor of RBI Raghuram Rajan wants action and whose list he submitted to PMO as early as 2015 in Modi Govt tenure. It failed to incite any action on part of Govt who instead of taking action against them kept on insisting even after Chief Information Commissioner (CIC) orders that they can’t even reveal names of these willful defaulters what to talk about recoveries. It is such actions which give hints to the willful big defaulters that the government is on their side and they have nothing to worry. The resultant compromised credit culture due to political impunity can also be smelled from record increase in bank frauds during Modi era. It is not only names of Vijay Mallya, Nirav Modi, Mehul Choksi that has become household names as they escape easily under patronage of Modi Govt but the record increase in bank frauds which highlights that fraudsters have nothing to worry. The bank frauds jumped exponentially to reach Rs 1.13 lakh Crore in first half of FY 2020 while it was pegged at mere Rs 10,170 Crore for whole year in 2013-14 when Modi Govt came to power. Its more than 10 fold increase even when the data for whole year is still not available for current fiscal. (Economic times). The Non-Performing Assets (NPAs) under Narendra Modi’s flagship scheme Pradhan Mantri Mudra Yojana(PMMY) saw a jump of 126% in just one year. The NPAs of loans issued under the programme leapt Rs 9,204.14 crore in FY 19 from Rs 7,277.31 crore in March 2018 to reach Rs 16,481.45 crore in March 2019.

It’s the combination of all this which explains record fivefold increase in NPA’s from 2014 to 2019 under Modi Govt to cross Rs 10 lakh Crore in 2018 only to improve marginally in 2019. It’s not only at stage of repayment but also at recovery stage that the institutional system in place put by Modi dispensation in form of Insolvency and Bankruptcy Code (IBC) and National Law Company Tribunal (NLCT), that give willful defaulters reasons to rejoice and behavioral tendencies to default on repayments.

NPA’s jumped five times to cross Rs 10 lakh Crore under Modi regime

Bank Frauds jumped more than ten times to reach unprecedented Rs 1.13 lakh Crore just in first half of FY 2020

NPAs under Mudhra stands at Rs 16, 481 Crore

IBC & NLCT: Banks run on depositor’s money take haircut, willful defaulters come clean

Under recovery process at play presently under much touted structural measures it’s the PSBs and banks in general, who runs on depositors money, that are being forced to take big haircut (financial jargon for write-offs) in such recoveries in name of speedy and streamlining of process. While govt wants us to believe that recovery rate at 43% has improved in last year, the truth is that this is half side of the story. The sheer scale of write offs are such that the PSB’s and banks in general will be forced to take a big haircut. As per business standard the cases referred to IBC increased 27 percent in volume while tripling in value in last financial year. In FY 19 around Rs 8.15 lakh crore worth of stressed assets were involved in recovery process up from Rs 2.7 lakh crore in FY 2017-18. Moreover the claimed marginal improvement to 43% in FY 19 was one off in nature due to improved comparative recovery in two-three big cases because of specific nature of them while in general the recovery rates remained low with banks forced to take big haircuts. After that it came down to just 12% in last December quarter of this financial year while it was 34% in quarter ending in September (Economic Times).

In FY19 Rs 8.15 lakh Crore worth of stressed assets under new IBC regime, up from Rs 2.17 lakh crore in FY18

Recovery rates stands at just 12% for quarter ending in December, 2019

The much celebrated earlier identification of NPA’s and initiation of timely recovery process then merely becomes a pretext to force the PSB’s to give up voluntarily on their legal debt claims while taking a big haircut, the brunt of which would obviously be borne by public at large whose money is being given up. In name of clean balance sheets for banks and debtors what is being siphoned off is public money and legal right to recover debt from willful defaulters. It won’t be out of order to point out that as per IBC, 2016, once proceedings have been initiated against a borrower under the IBC, the Sarfaesi Act cannot be invoked against them which have much stringent provisions for recovery and criminal action against willful defaulters. Similarly, if an errant borrower was being pursued under the Sarfaesi Act before the IBC came into effect, and the lender now wants to initiate proceedings under the IBC, the Sarfaesi proceedings would cease to apply to the borrower. It’s here that cronies close to ruling dispensation will get a big pie of the forced haircut while coming out clean after completion of the celebrated timely and speedy recovery process! Can you imagine any bank giving up voluntarily on say even half of amount of home loans and car loans for small time genuine borrowers in practice even if they fail to pay EMI’s say due to loss of employment?

Claim of improvement in NPAs only half truth

Despite tall claims by Central Govt that 2019 seems as turning around year for banking sector in form of a little improved ‘recovery rates’ and lowering of NPA’s, the risk of full fledged financial crisis persists. The NPA’s in banking sector continues to hover at dangerous level and a little improvement that is talked about is mainly because of moratorium put on classification of debt of small and medium enterprises as NPAs. It is this sector which has taken maximum hit due to disastrous policies of demonetization and GST and its only when moratorium on classification of debt as NPA’s is lifted for them in March 2020, unless extended, that the real picture of state of NPA’s can emerge. While on one hand the moratorium is in name of helping small and medium businesses by not classifying their assets as NPA’s, the other side of the story is that it’s the big businesses and big corporates who gets the first opportunity to milk the recovery process at IBC and NLCT. It will result in a situation that willful big corporate defaulters abuse the process while small and medium sector borrowers who genuinely defaulted due to effect of economic downturn on its business are denied opportunity of debt settlement opportunity.

Innocent depositors most hard hit

As happens in every such fiasco it’s the innocent depositors’ who keeps their hard earned money in banks, keeping faith on regulatory process of RBI and Govt in place, who takes the brunt while the cronies and willful defaulters sees opportunity to emerge out of it with ‘clean balance sheets’. The story of Yes bank depositors’ is no different. While 21 lakh of ordinary depositors faced moratorium on withdrawal as they found out that there deposits were used to lend loans without basic due diligence by management while the regulatory bodies were seeing other way when all this was happening with their money in last few years. They now found out that as much as Rs 21,000 Crore are stuck with Anil Ambani group (Rs 12,800 Crore) who was favoured during Rafale deal by Modi Govt and Subhash Chandra owned Essel group (Rs 8,400 Crore) which control Zee news, widely believed as mouthpiece of BJP government. It is being told that ten big defaulters debt amount to whopping Rs 36,000 Crore and besides two mentioned above includes names such as DHFL Group, IL&FS, Jet Airways, B M Khaitan Group, Omkar Realtors (Deccan herald). Many of these names were already making news for wrong reasons and bad financial health in past but were able to avail credit from Yes Bank. The loan book of Yes bank jumped from around Rs 55,000 Crore in 2014 to staggering Rs 2, 41,000 Crore in March 2019 within span of five years with most dramatic rise coming in two years post demonetization with jump of more than Rs 1 lakh crore in loan book with no one in RBI and Govt raising the alarms. It is these unrestrained lendings which have now become stressed with fear of financial loss hanging on innocent depositors.

Restructuring plan: Use of public money to bail out banks without fixing responsibility on willful defaulters

The protagonist of Modi govt claims that depositor’s money is safe but who is footing the bill of this safety which should be asked? The depositor’s money became insecure in first place due to culture of political impunity enjoyed by willful defaulters but the restructuring plan in place hovers around public funded SBI headed consortium of investors to bail out Yes Bank with SBI picking up 49 percent stake at Rs 7,250 Crore. Other private sector players such as Axis Bank Ltd., ICICI Bank Ltd. Kotak Mahindra Bank, Bandhan Bank and Federal Bank as well as housing finance company Housing Development Finance Corporation Ltd have also approved investments in Yes Bank. But its pertinent and ironical to note here that at the same time when SBI is being asked to foot the bailout bill the bank slashes interest rates on saving and term deposits. Thus loss of Rs 6,754 Crore in interest to 44 Crore of ordinary savings and term deposit holders of SBI would now be utilized to fund Rs 7,250 Crore bailout investments in Yes bank, the need of which arose due to likes of cronies like Anil Ambani and Subhash Chandra defaulting on loans from Yes Bank. This is not first time that public money of SBI which is being used to bail out erring private sector bank as govt gears its act to rescue depositors to address crisis. Last year it was LIC who was forced to put in Rs 21,000 Crore in IDBI. This amounts to use of public money in name of securing particular set of depositors while the willful defaulters would be in position to milk the cake through IBC and NLCT route when recovery process would be unleased for defaults in such failing banks including Yes bank. The restructuring for banking sector as a whole to address NPA crisis has taken the form of recapitalization from budget resources to the tune of around Rs 2.5 lakh Crore from 2015 which is obviously tax payer’s money. The situation had become so worse that to balance the budget and foot recapitalization bill the govt has even drawn on reserves of RBI.

The deposits of Yes Bank had already plummeted in last year as news of bad financial health was doing the rounds. It is difficult to imagine how depositor’s confidence would be regained now when the news of complete fiasco is now in open. The depositors are likely to withdraw money for safety once moratorium is lifted. The ideal thing even in such crisis would have been that SBI should have completely taken over Yes Bank as was practiced earlier in case of Global Trust Bank so that with brand of SBI depositors of Yes bank would have felt secured and their interest completely protected. It’s even more essential when one takes into account the fact that PMC depositors have still not being paid off and they even failed to secure relief from Bombay High Court. Legally also the depositors insurance extend only to cover of Rs 1 lakh of their deposits in each bank.

Public money utilized for restructuring due to banking crisis:

LIC puts Rs 21000 Crore in IDBI

SBI puts Rs 7,450 Crore in YES BANK

Slashing of Interest rates to fund investments in Yes Bank costs ordinary depositors Rs 6,754 Crore

Recapitalization of banks through budgetary resources reached Rs 2.5 Lakh Crore

Conclusion:

The Yes Bank and banking crisis in general has its roots in crony capitalism and neo-liberal policy framework. Recapitalisation and bail out of banks has become a cover for stealing of people’s money through multiple routes - claiming RBI reserves several times, forcing PSBs and LIC to invest in faultering banks, direct use of tax payers’ money through budgetary resources for capital infusion, bleeding the depositors through steady cuts in deposit rates, multiple charges for banking services etc. This all is in essence only to compensate and make up for the loans given out of common people’s deposits that corporates and cronies have happily walked away either as NPAs, unrecovered loans, write offs, or even through pure fraud, and all with full political impunity.

The real intention of recently announced govt plan of mergers of PSBs is also to utilize the public money and depositors’ money in most ‘efficient’ way to achieve the objective of ‘clean balance sheets’ of willful defaulters to safeguard them at time of economic crisis while legally writing off their debts in name of timely settlements and recovery process. The government’s want that PSBs run on public money- both of depositors and people in general who pay taxes to govt- mainly bear the brunt of defaults by big corporates and thinks that merged ‘strong’ PSBs would be in better position to survive these forced haircuts. It eventually plans to privatize them as banks with better logistics, integrated wide branch network, lean organization with reduced staff strength after mergers and package them as lucrative offers to international financial capital and big MNCs and Corporate houses as banks with ‘clean’ balance sheets. But what in essence is cleaned is public money in general, depositors money and employment at PSBs as willful big defaulters come out clean out of the crisis with help of IBC and NLCT. It’s unlikely that it would be any different for Yes bank as the recovery process in place is available to defaulters of Yes Bank too like other defaulters. The essence of the policy framework in place thus is to push the burden of economic crisis on people’s throat and eventual privatization of PSBs as restructuring of financial and banking sector- part of second generation reforms- with demonetization earlier only providing the much needed liquidity in banks to keep them float during pressing times. Cronies in end relish, while public funds (Jandhan) perish!

Charu Bhawan, U-90, Shakarpur, Delhi 110092

Phone: +91-11-42785864 | Fax:+91-11-42785864 | +91 9717274961

E-mail: info@cpiml.org